Personal finance in India is changing every passing day, and the people who will treat money like a system will stay ahead in the race. For an Indian earner today, getting the basics right is no longer optional, it is survival. It involves budgeting, protecting against shocks, and investing smarter than inflation.

- What is personal finance

- Why personal finance matters

- Steps for effective personal finance

- Step 1: Build a realistic budget

- Step 2: Prioritize an emergency fund

- Step 3: Control unnecesary debt

- Step 4: Start investing early and consistently

- Step 5: Align your investment with clear goals

- Step 6: Use tax rules and digital tools wisely

- Step 7: Have necessary insurance

- Step 8: Build skills, keep learning

- Conclusion

What is personal finance

Personal finance is the process of planning and managing your financial activities, including budgeting, saving, spending, investing, and protecting assets to achieve you future goals. Personal finance helps you plan how to use your money so you can meet your needs today and your goals tomorrow without running into money troubles. It’s like a roadmap for handling your money smartly, so you feel secure and confident about your financial future.

Why personal finance matters

In todays world cost of living, education fees, and housing costs have been rising consistently, which means your income must grow and your money must be managed well just to maintain your standard of living. At the same time, digital payments, easy credit, and online investing have made it both easier to grow wealth and easier to make irreversible mistakes.

For a typical Indian salaried professional or small business owner, personal finance is not about getting rich quickly; it is about ensuring that every rupee earned has a clear job. It may be used for paying for today, preparing for emergencies, and compounding for tomorrow.

Your peace of mind will depend on the things you do right at the moment. Your right steps will reduce stress, gives you more options in life, and helps you support family goals such as children’s education and parents’ healthcare with confidence.

Steps for effective personal finance

Step 1: Build a realistic budget

A budget is simply a plan for your monthly cash flow, and it is the foundation of all financial decisions. Without it, even a high income can disappear into EMI payments, impulse spending, and unnoticed subscriptions.

Many Indian experts recommend simple frameworks like the 50‑30‑20 rule: around 50% of income for needs, 30% for wants, and 20% for savings and investments, which you can tweak based on your life stage. You can start by listing all income sources, then categorising expenses into essentials (rent, groceries, school fees, EMIs) and discretionary spends (eating out, shopping, subscriptions) using a notebook, spreadsheet, or some finance expense apps.

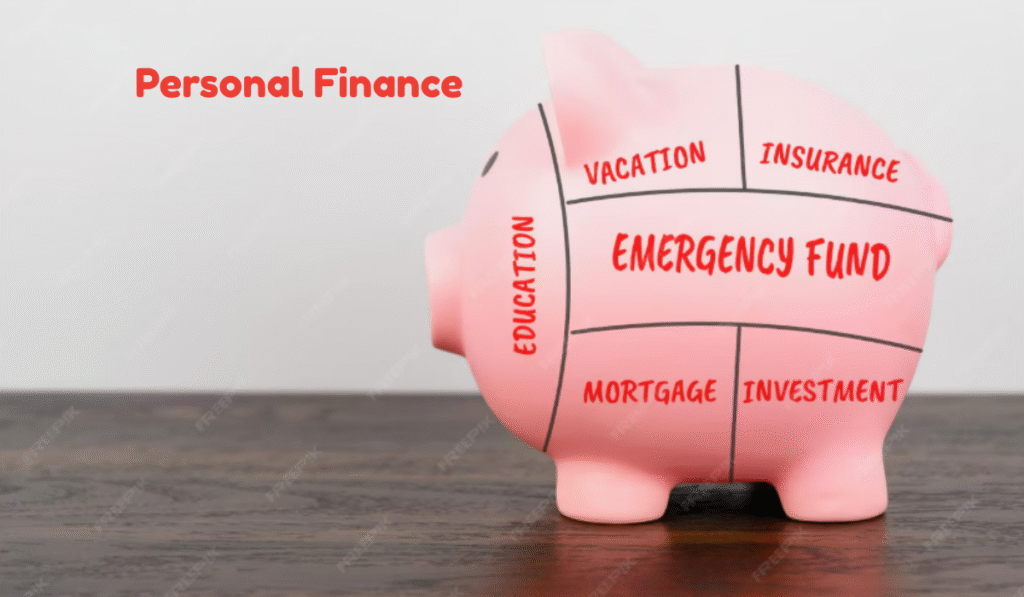

Step 2: Prioritize an emergency fund

Before chasing high returns, every Indian household needs a safety buffer for unpredictable events like job loss, medical emergencies, or sudden repairs. This emergency fund stops you from swiping credit cards or taking personal loans at very high interest when life goes wrong.

A common thumb rule is to keep 3 to 6 months of essential expenses in a liquid, low‑risk place like a savings account or liquid mutual fund which can be easily accessible whenever needed. You can start with minimum amount initially and automate it to build the fund slowly. The peace of mind it provides is worth more than the modest returns.

Step 3: Control unnecesary debt

In India, easy EMIs and credit cards can quietly erode your future wealth if not handled carefully. High‑interest debt, especially credit card dues and personal loans, grows much faster than most investment returns.

Two common strategies to get out of debt are the “avalanche” method where you pay highest interest loan first, and the “snowball” method where you close small loans first. Whichever you choose, the key is to stop adding new unnecessary debt, pay at least the full statement amount on credit cards each month, and avoid converting every purchase into long‑tenure EMIs that eat up your future cash flow.

Step 4: Start investing early and consistently

Saving is not enough in an environment where inflation reduces the value of money every year; your money needs to grow faster than inflation and taxes. For most Indians, that means combining safe vehicles for stability with growth‑oriented investments for long‑term goals.

Some common options include savings accounts and fixed deposits for capital protection, equity and hybrid mutual funds for long‑term growth, PPF and NPS for tax‑efficient, long‑horizon wealth building, and a limited allocation to assets like gold for diversification. The exact mix should depend on your risk tolerance and goals, but starting early with even small SIPs can harness the power of compounding over the period of 10 to 20 years.

Step 5: Align your investment with clear goals

Money decisions feel confusing when there is no clear purpose behind them, so defining goals is a crucial part of personal finance. These can include short‑term targets like building a ₹1 lakh emergency fund, medium‑term goals like a car down payment, and long‑term goals like retirement or a child’s higher education.

Once the goals and timelines are clear, you can choose products that match you goals. Reviewing these goals at least once a year helps you adjust contributions, rebalance investments, and stay on track despite market volatility or life changes.

Step 6: Use tax rules and digital tools wisely

The Indian tax system offers several incentives for people who plan ahead, which can significantly improve net returns if used correctly. Deductions under sections like 80C and 80D, and products like PPF, NPS, and ELSS funds, can simultaneously reduce taxable income and grow wealth over time when used as part of a holistic plan rather than last‑minute March investments.

Digital platforms, online broking, and other finance planning apps have made it easier to track expenses, invest in mutual funds or stocks, and monitor goals from a smartphone. However, convenience should not replace due diligence, so it remains important to verify costs, read product disclosures, and avoid chasing every new trend or tip seen on social media.

Step 7: Have necessary insurance

Your emergency fund might not be sufficient during the unexpected health issues like medical expenses, disabilities by accident or death. This is where insurance acts as a safety net, protecting your money and family from big unexpected losses.

In personal finance planning, insurance provides peace of mind, tax advantages (like deductions on premiums), and liquidity for emergencies. Every Indian should have health and life insurance to protect against rising medical costs and family responsibilities.

Assess your needs by calculating coverage for 10 to 15 times annual income for life insurance and 3 to 6 months expenses for health insurance. Always go for simple term plan for life insurance and family floater for health insurance. You may opt for riders based on your needs.

Step 8: Build skills, keep learning

Finally, personal finance is not only about squeezing more out of your existing salary but also about increasing your earning capacity over time. In an economy where inflation, currency depreciation, and taxes all eat into real wealth, developing skills that improve your income is a powerful financial strategy.

Investing in professional courses, certifications, or digital skills can raise your income potential, while maintaining discipline against “lifestyle inflation” ensures that higher income actually translates into higher savings and investments. This combination of higher earning power, controlled spending, and systematic investing, is what gradually shifts an Indian household from financial stress to financial confidence.

Conclusion

Personal finance empowers you to take control of your money, turning everyday earnings into lasting security and freedom through smart budgeting, saving, investing, and protection.

If you haven’t started yet then start today by tracking your expenses, building an emergency fund, and investing small amounts consistently. The small habits you start today may compound into financial independence over time.